A Fat Bank Balance Won't Get You a Visa. Here's What Actually Does.

A big number in the passbook is not the magic key to a visa. Officers approve genuine, available, well-explained money — plus your ties and purpose. Here's how to prepare funds that help your case instead of sinking it.

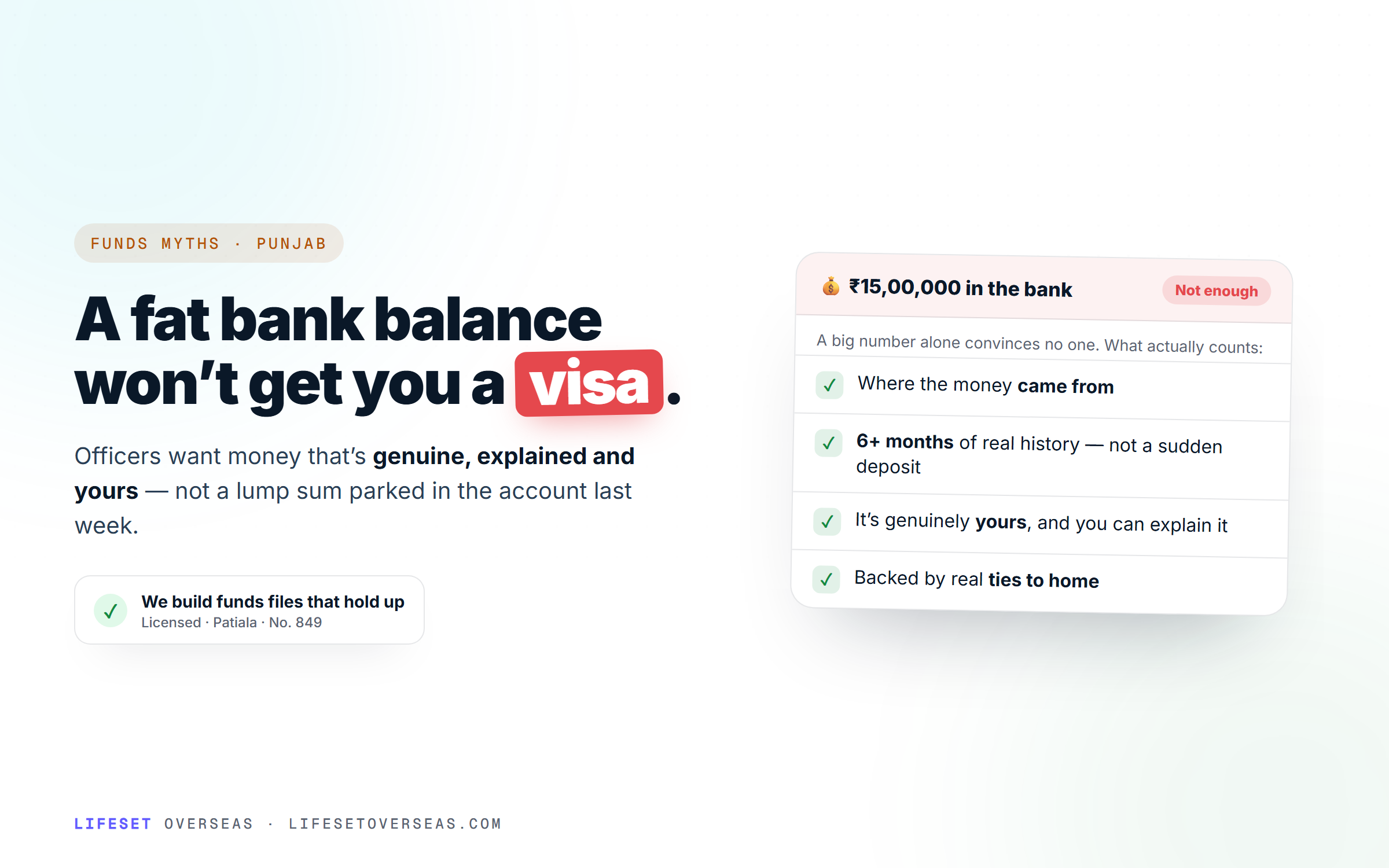

Walk into any Patiala bank in visa season and you will hear the same request across the counter: "Bhai, I need to show a big balance for my Canada file — can you park some money in my account for a month?" It is one of the most stubborn beliefs in Punjab: that a fat number in the passbook is the magic key that unlocks a visa.

It is not. A visa officer does not approve a balance — they approve a story, and money is only one line of it. As a licensed consultancy that reads refusal letters every week, we can tell you plainly: a large, unexplained deposit that landed last Tuesday does more damage than a modest, genuine balance you built over a year. Here is what an officer actually looks for, and how to prepare your funds so they strengthen your case instead of sinking it.

The myth: a big balance is not the same as genuine funds

The passbook screenshot is only a photograph of one moment. It tells the officer nothing about where that money came from, whether it is really yours to spend, or whether it will still be there next week. Visa sections around the world are trained on exactly this — spotting money that was arranged for the file rather than owned by the family.

The uncomfortable truth is that a genuine ₹6 lakh you have grown steadily is worth more to your file than a borrowed ₹25 lakh that appeared overnight and will vanish the moment the decision lands.

What officers actually test on your money

Before we get to the tricks people try, it helps to know the real thresholds — because guessing is how files fail. These are the current official figures for the routes Patiala families ask about most.

CA$22,895

Canada study permit — living costs

Single applicant, outside Quebec, from 1 Sept 2025. On top of first-year tuition and airfare.

£1,529/mo

UK student visa — London living costs

Up to 9 months; £1,171/mo outside London. Held 28 days straight.

€120/day

Schengen (France) — daily funds

Without prepaid stay; drops to €65/day with a confirmed hotel booking.

Hitting the number is only the entry ticket. Once your balance clears the threshold, an officer runs it through three quiet questions:

Is it genuine? Did this money grow through real income and savings, or did it appear to satisfy a requirement?

Is it available to you? Can you actually access and spend it, or is it locked in someone else's account or a fixed deposit you cannot touch?

Is it explained? Can every significant credit be traced to a lawful, believable source?

Fail any one of those and the balance stops helping — no matter how large it is.

"Seasoning": why last-minute lump sums fail

Fund seasoning simply means money that has sat in the account long enough to look like it belongs there. Consulates do not just want a today balance — they want history.

The UK 28-day rule

→

28 consecutive days

Source: GOV.UK — Student visa: money you need

For a UK student visa, your maintenance money must sit in the account for 28 straight days, it cannot dip below the required amount on even a single day of that window, and the 28-day period must end no more than 31 days before you apply. Schengen posts routinely ask for the last three to six months of bank statements, precisely so a one-week spike stands out. Canada — now that the Student Direct Stream has closed and everyone applies through the standard stream — expects the same logic: a believable financial history across your recent statements, not a freshly loaded account.

This is why timing beats amount. A steady balance held quietly for three to six months tells a far better story than a bigger number parked for a fortnight.

Source of funds: where did the money come from?

The question behind every large credit is simple: where did this come from? If you cannot answer it on paper, the officer will answer it for you — usually unfavourably.

Sponsor credibility is the other half of this. A father who is a salaried government employee, or a farmer with documented agricultural income and land records, is a believable sponsor. An uncle who "will fund everything" but whose own accounts show no capacity to do so is not — and naming him can weaken, not strengthen, your file. Match the money to a person who can plausibly have earned it.

The real numbers, so you are not guessing

Current proof-of-funds benchmarks (verify before applying)

Canada — study permitLiving-cost figure applies from 1 Sept 2025; it sat at CA$10,000 for roughly 20 years before back-to-back rises.

CA$22,895 living costs + first-year tuition

UK student — in LondonPlus any outstanding tuition; funds held 28 consecutive days.

£1,529/mo × up to 9 months ≈ £13,761

UK student — outside LondonPlus outstanding tuition; same 28-day holding rule.

£1,171/mo × up to 9 months ≈ £10,539

Schengen visitor (France)€32.50/day if staying with a host under a validated attestation d'accueil.

These are the floors, not comfortable targets. Sitting a little above the minimum with a clean history is far stronger than towering over it with money you cannot explain.

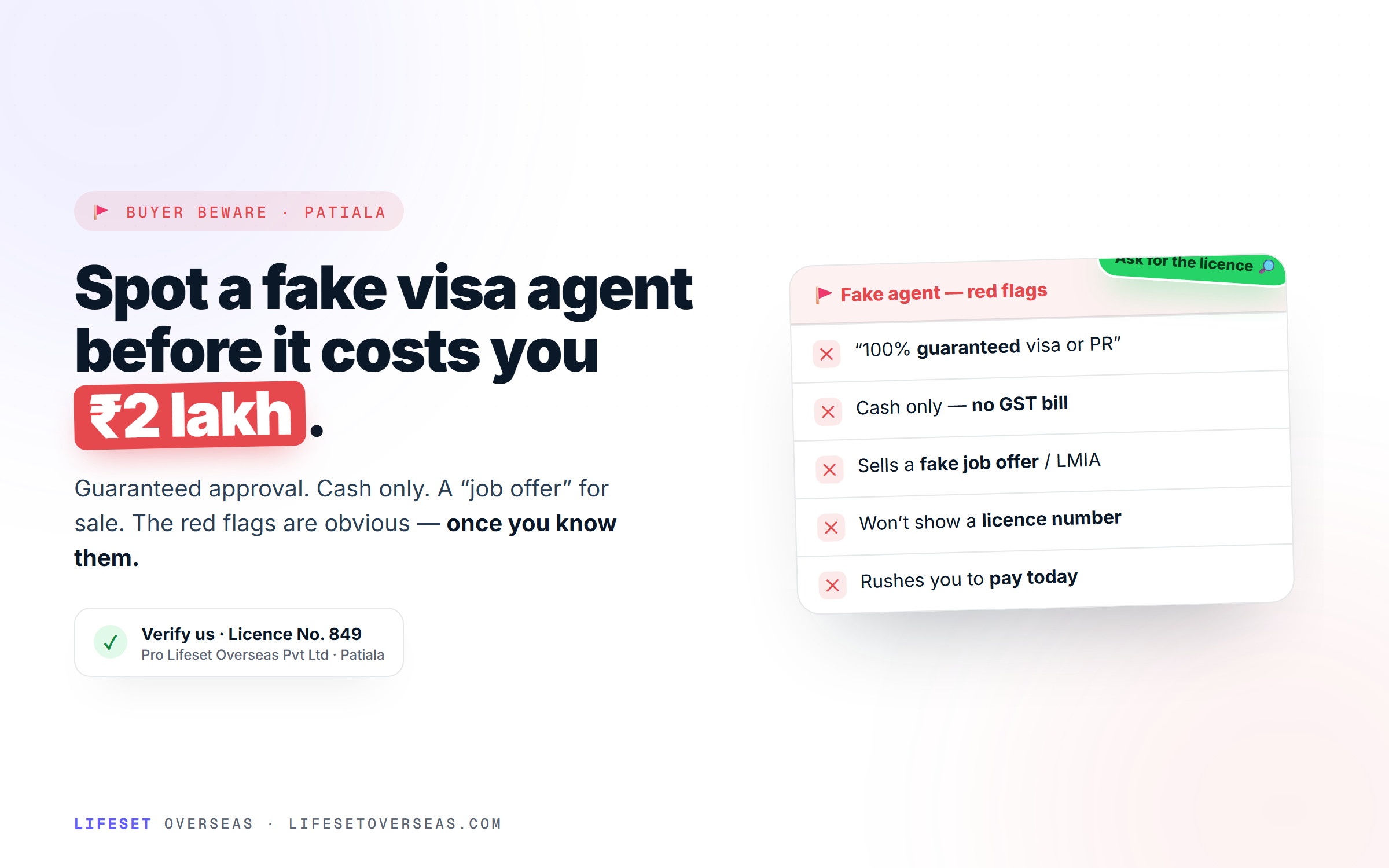

The fund mistakes we see most in Patiala

No. 1

The last-minute lump sum

Loading the account days before applying is the classic error. It is the first thing an officer notices and the fastest way to have your whole financial picture treated as arranged rather than owned.

No. 2

The unexplained deposit

A large credit with no matching payslip, sale deed or gift paper. If you cannot document where it came from, assume the officer will read it as borrowed or arranged.

No. 3

Money in the wrong name

Funds sitting in a cousin's account, or locked in an FD you cannot break in time, are not "available" to you. Show money you can actually access, or a properly documented sponsor relationship.

No. 4

Borrowed funds returned after the file

Parking a friend's or agent's money for the statement, then sending it back, is exactly the pattern verification checks are built to catch — and it can taint every future application too.

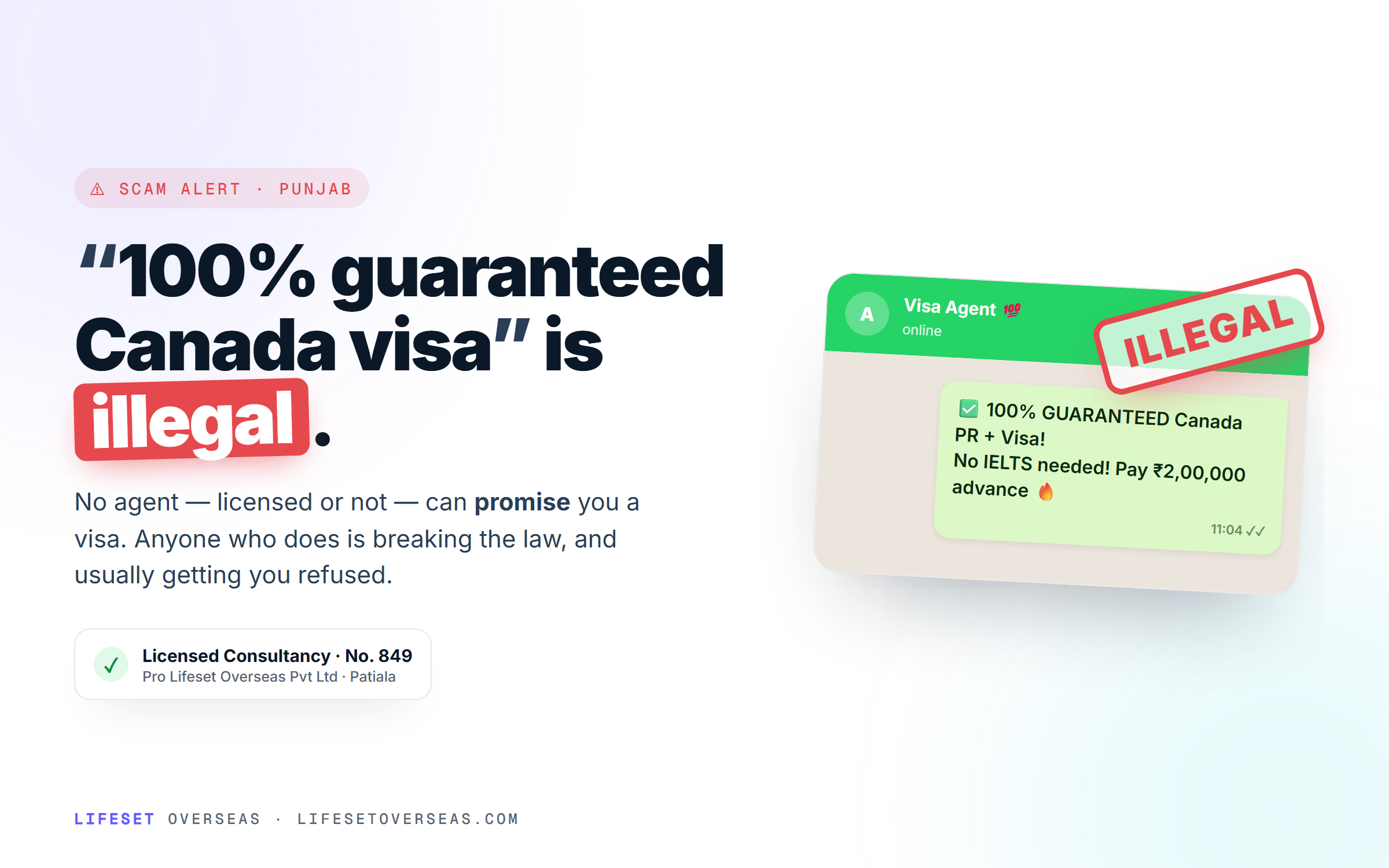

We turn away these shortcuts when families ask for them, because a clean refusal reason today becomes a credibility problem on every file you ever submit afterwards.

Money proves capacity — not intent

Here is the part the "big balance" belief misses entirely. Your funds only answer one question: can you afford this trip? They say nothing about the two questions an officer cares about just as much — is your purpose genuine, and will you respect the visa's conditions?

1

Start early, season the funds

Build and hold your balance for three to six months before applying. Time in the account is worth more than the size of the deposit.

2

Document every large credit

For each significant deposit, keep the proof — payslip, ITR, sale deed, or a gift declaration — ready to submit alongside the statement.

3

Pick a credible sponsor

Fund the trip from someone whose own income clearly supports it, and include that sponsor's financial documents, not just yours.

4

Leave the money untouched

Do not make big withdrawals or transfers during the statement window. A steady line reassures; a jagged one invites questions.

5

Pair funds with ties and purpose

Show what pulls you home — a job, family, property, an ongoing business or course — and a clear, honest reason for the trip. Money plus roots beats money alone.

A visitor with a modest, well-explained balance, a stable job in Patiala and a specific reason to travel is a stronger applicant than someone flashing a huge number with no ties and no story. The balance opens the door; your genuineness walks you through it.

Frequently asked questions

Does a bigger bank balance improve my chances of a visa?

Not on its own. Once you clear the minimum, extra money adds little if it cannot be explained. Officers weigh whether funds are genuine, available and documented — and then weigh your ties and purpose. A clean, seasoned balance at the threshold usually beats a huge, unexplained one.

How long should money sit in my account before I apply?

As long as you can, ideally three to six months. The UK student route formally requires funds to be held for 28 consecutive days, ending no more than 31 days before you apply, and Schengen posts routinely read three to six months of statements. A longer history reduces the risk your money looks arranged.

Can my parents or a relative sponsor my visa?

Yes, and it is completely normal — but the sponsor must be credible. Include their income proof (ITRs, salary slips or business documents) and a short declaration of support. The officer needs to believe the sponsor genuinely earned the money and can afford to give it.

Why would a large deposit hurt my application?

Because a sudden, unexplained jump reads as "window dressing" — money arranged for the file rather than owned by the family. It can make the officer doubt not just your funds but the honesty of your whole application. A documented source turns that same deposit from a red flag into an asset.

Is there a fixed minimum bank balance for a Schengen visitor visa?

There is no single figure across all countries, but each state publishes a daily rate. France, for example, expects €120 per day without prepaid accommodation, €65 with a hotel booking, or €32.50 if a host proves your stay with a validated attestation d'accueil. Germany works on roughly €45 per day, with no fixed amount set per consulate. Always check the specific country's rate for your dates.

Can Lifeset Overseas guarantee approval if my funds are strong?

No — and be wary of anyone who does. The decision belongs entirely to the visa officer. What we can do is help you present genuine, well-seasoned, properly documented funds alongside solid ties and a clear purpose, so your file is as strong and honest as it can be.

Money is the part of a visa file people worry about most and understand least. If you would rather build a clean, believable financial story than gamble on a last-minute lump sum, come and talk to us. Our licensed team can review your bank statements, sponsor documents and ties before you apply, and flag the problems a visa officer would.

Walk in to our Patiala office at Shop No. 2, Nabha Road, near PRTC Workshop — we also serve families across Rajpura, Nabha and Sangrur. If a previous refusal mentioned funds, our visa refusal support and GCMS/CAIPS notes service can tell you exactly what the officer flagged. Prefer to write it down first? Our SOP writing team can tie your funds, purpose and ties into one honest narrative. Call or WhatsApp us on +91 91155 80911 in Punjabi, Hindi or English — we would rather fix your file before you apply than after a refusal.

Talk to a consultant about your case

Read this article? Now tell us about your situation.

We’ll WhatsApp you within 4 working hours with an honest read on your file and the realistic next steps. licensed, fixed-fee, one consultant from first call to decision.

WhatsApp: · usually faster.

One message away

Talk to a consultant about your case

Read the article? Message us on WhatsApp with your situation — a licensed consultant gives you an honest read and the next step.